Navigating and Avoiding Pre-Foreclosure in Las Vegas

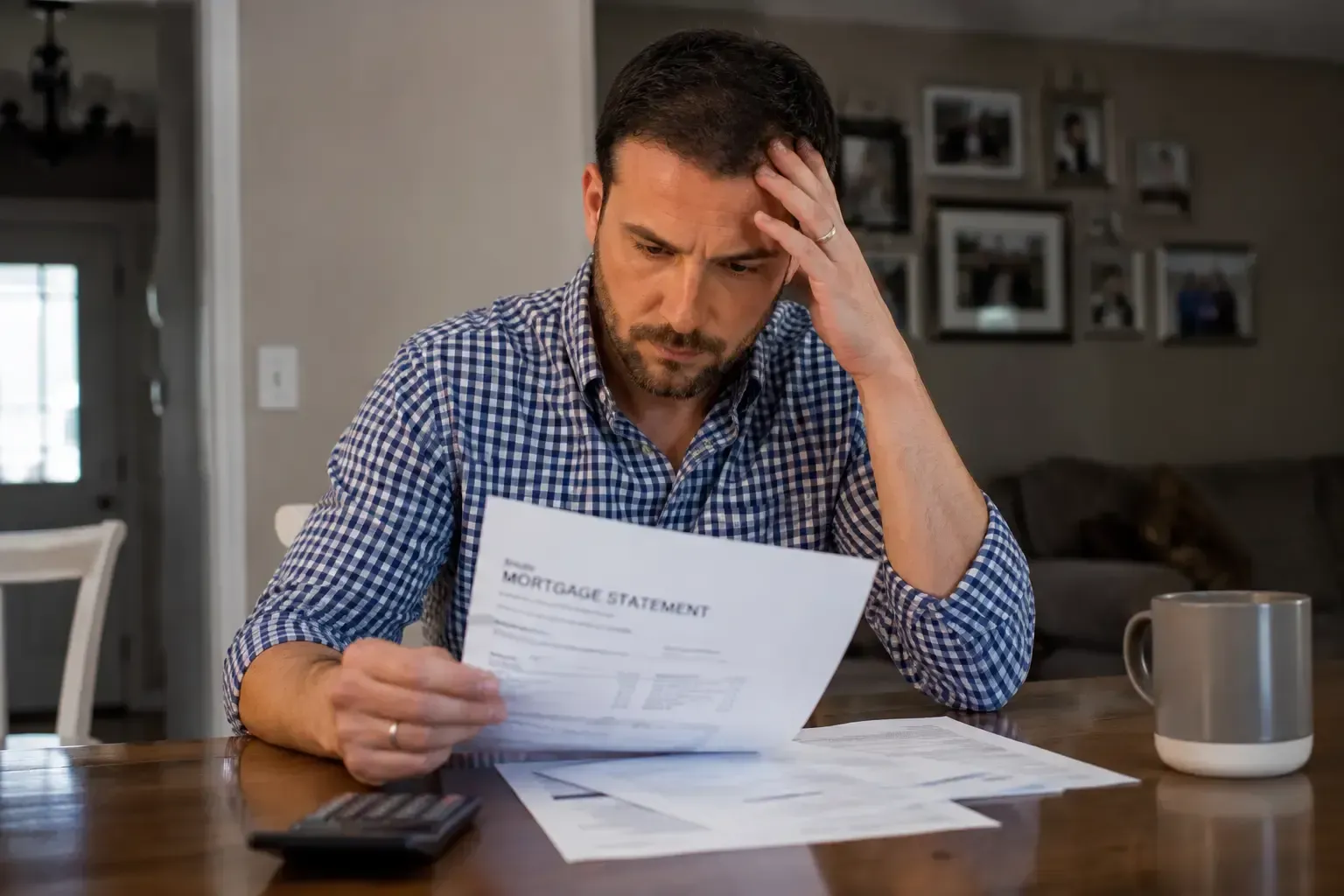

Falling behind on mortgage payments causes immense stress for any homeowner. In Las Vegas, NV, the local housing market moves rapidly. When missed payments start piling up, lenders take action. This initial stage is known as pre-foreclosure. It serves as a warning period before the bank officially repossesses the property. Many homeowners feel completely paralyzed during this time.

The good news is that receiving a notice from your lender does not mean losing your home is inevitable. You have legal rights, viable options, and proven pathways to protect your financial future. At Las Vegas Sell House Fast, we work directly with property owners to find logical exits before the bank takes total control.

Understanding the Pre-Foreclosure Timeline in Real Estate

Nevada operates primarily as a non-judicial foreclosure state. This means lenders do not need to go through the court system to take back a property. The timeline moves faster here than in many other states. Once you miss a few consecutive payments, the lender records a Notice of Default with the Clark County Recorder. This public document officially starts the clock.

From the recording date, Nevada law mandates a strict waiting period. Homeowners generally have a limited window to make up the missed payments, negotiate with the bank, or sell the property. Ignoring the letters or phone calls will only accelerate the process. Property owners must confront the situation immediately.

If you already feel overwhelmed with property problems, Las Vegas sellers have a faster way out. Taking decisive action during this specific grace period dictates whether you walk away with cash in your pocket or a severe hit to your credit score.

Immediate Steps to Protect Your Las Vegas Home

The moment you realize making the next mortgage payment is impossible, you must shift into problem-solving mode. Silence is the worst strategy you can employ. Lenders prefer to avoid foreclosing on residential properties because the legal process costs them considerable time and money.

Here are the specific actions you should take right away:

- Contact the Loss Mitigation Department: Call your lender and ask for this specific department. Explain your financial hardship clearly and honestly.

- Request a Forbearance: If your financial hurdle is temporary, the lender might agree to pause or reduce your payments for a few months.

- Apply for a Loan Modification: You can ask the bank to restructure your loan terms. This might involve extending the life of the loan or lowering the interest rate to make monthly payments manageable.

- Review Nevada Foreclosure Mediation Rules: Nevada offers a Foreclosure Mediation Program. Enrolling in this program forces the lender to sit down with you and a neutral mediator to discuss alternatives to repossession.

While these options exist, they require heavy paperwork and strict compliance. If the bank denies your requests, you must have a backup plan ready.

Strategies for Halting Bank Action Permanently

When keeping the house is no longer financially viable, selling the property becomes the most logical step. A strategic sale allows you to pay off the mortgage, satisfy the lender, and move forward. Avoiding pre-foreclosure through a sale comes in a few different forms.

A short sale occurs when the bank agrees to let you sell the home for less than the outstanding mortgage balance. This requires specialized lender approval and can take months to finalize. Retail buyers often back out of short sales due to the lengthy bureaucratic delays.

Selling to a direct cash buyer eliminates those delays entirely. In Las Vegas, professional buyers can assess the property, make an offer, and close within a matter of days. You bypass the need for costly repairs, professional staging, or real estate agent commissions. This speed is critical when the Notice of Default clock is ticking. This exact strategy applies to both standard homes and commercial properties facing financial distress.

The Financial Impact of Bank Repossession

Allowing a property to go through the complete repossession process leaves lasting scars on your financial record. A finalized foreclosure stays on your credit report for up to seven years. This makes renting an apartment, securing auto loans, or buying another house extremely difficult. Furthermore, it can impact your security clearances or employment prospects depending on your specific industry.

In some cases, lenders may even pursue a deficiency judgment to collect the remaining balance if the house sells at auction for less than what you owe.

Taking control of the sale before the auction date protects your credit rating from that devastating blow. Selling proactively demonstrates financial responsibility to future creditors. If you want to learn more about how our team facilitates these rapid transactions, read about our proven process. We understand the local Las Vegas market and the strict urgency required to beat bank deadlines.

Taking Control of Your Property Dilemma

Time remains your most valuable asset when dealing with a pending bank action. Every single day that passes narrows your available choices. You need a clear understanding of your property value and a realistic assessment of the timeline you are working against.

Gather your loan documents, calculate your exact payoff amount, and explore all available financial avenues. If listing the house on the traditional market will take too long, securing a cash offer provides an immediate safety net. Reach out to Las Vegas Sell House Fast to discuss your unique timeline. You can easily contact our local team for a confidential property evaluation. We provide transparent, fair offers designed to help you bypass the auction block entirely.

Frequently Asked Questions

How long does pre-foreclosure take in Nevada?

After the Notice of Default is filed, Nevada law requires a minimum 90-day waiting period before the lender can issue a Notice of Sale. The Notice of Sale then requires an additional 21 days before the public auction can legally occur.

Can I sell my house if I have received a Notice of Default?

Yes. You retain full ownership of your property during this entire phase. You are legally permitted to sell the home at any time before the scheduled public auction takes place.

Will selling to a cash buyer stop the foreclosure process?

Yes. If the sale closes and the outstanding mortgage balance is paid off before the auction date, the bank action stops immediately. The lender receives their funds, and your credit is spared from a finalized repossession mark.